I was going through the FICCI–Deloitte India Consumer Decade report while prepping for a DilSe Omni episode, and one number made me stop.

India’s retail market is projected to go from US$1.065 trillion in 2024 to US$1.93 trillion by 2030. That is nearly doubling in six years. To put that in perspective — India is adding the retail equivalent of Germany’s entire economy in less than a decade.

When a report comes out with FICCI and Deloitte behind it, you pay attention. This is not a startup whitepaper or a VC deck. This is the institutional view of where Indian commerce is heading. And what it says is both exciting and uncomfortable — because the next US$865 billion of growth will not look like the last. It will be concentrated in different channels, different cities, and different consumer cohorts. Brands that misread the pattern will think they are growing when they are actually falling behind.

In this blog, I want to break down the 10 signals from this report that every brand, retailer, and marketer in India needs to act on right now.

Table of Contents:

- Is India’s Retail Market Really About to Double — and What Does It Mean for Your Brand?

- Online Is Growing 2.5× Faster — So Why Does Offline Still Win the Absolute Rupees?

- Has Quick Commerce Already Become India’s Primary Digital Shelf?

- Are Kiranas Actually Dying — or Is Something More Interesting Happening?

- Is Your D2C Brand Ready for a Market That Triples to US$267 Billion?

- Is Bharat the Real Growth Engine Now — and Are You Building for It?

- Gen Z Has US$250 Billion — Are You Speaking Their Language?

- Social Commerce Is Growing 40%+ — Has Your Funnel Changed With It?

- Premium Is Growing Twice as Fast as Mass — Are You on the Right Side of That Split?

- AI, ONDC, and Omnichannel — Are These Still Pilots in Your Organisation?

- Conclusion

1. Is India's Retail Market Really About to Double — and What Does It Mean for Your Brand?

India’s retail market sits at US$1.065 trillion today. The FICCI–Deloitte report projects it reaches US$1.93 trillion by 2030 — a steady 10% CAGR. India is already the world’s fifth-largest retail market, contributing over 10% to GDP.

But headline growth numbers hide more than they reveal. The question is not whether the market will grow. It is where the growth concentrates — and whether your brand is positioned inside that concentration or outside it.

The next US$865 billion will be distributed unevenly. Different channels, different cities, different price points. Get the read right and you grow with it. Get it wrong and you underperform a booming market.

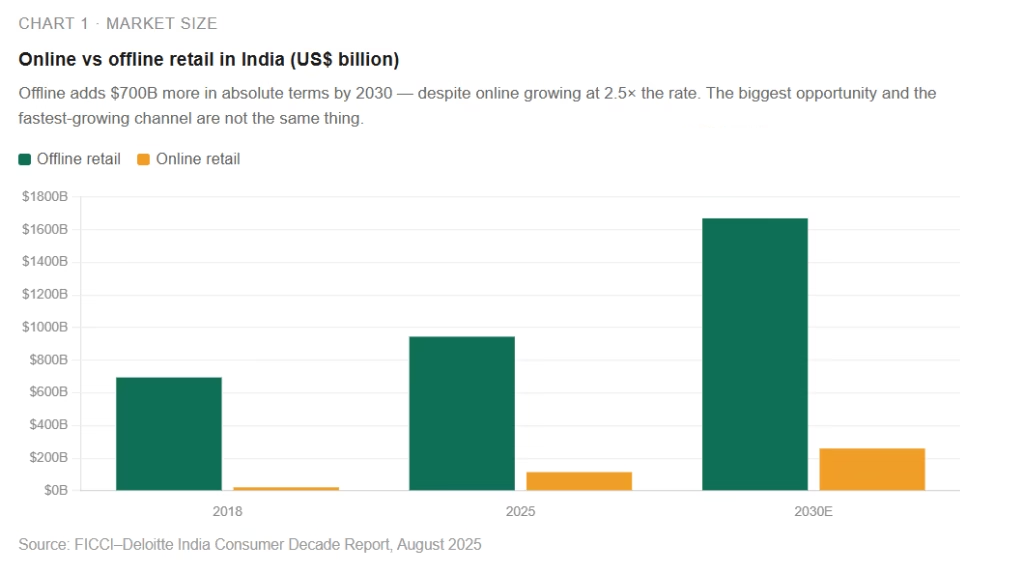

2. Online Is Growing 2.5× Faster — So Why Does Offline Still Win the Absolute Rupees?

This is the insight most brands get wrong.

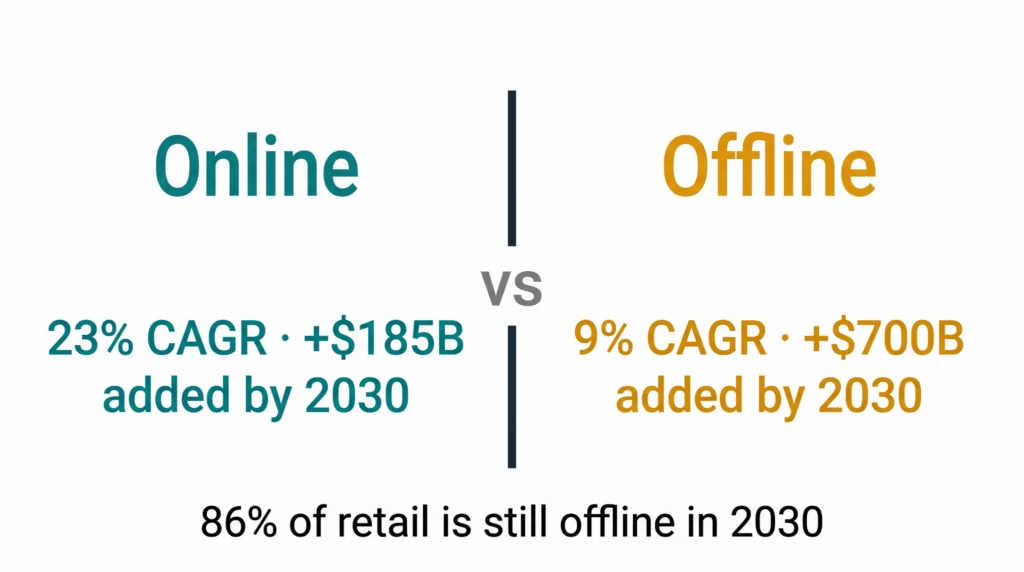

Online retail grows from US$75 billion today to US$260 billion by 2030 at a 23% CAGR. The fastest growth rate in any retail segment. So teams naturally chase it.

But offline retail adds US$700 billion in absolute terms over the same period. Online adds US$185 billion. Traditional retail still holds 86% share by 2030.

The highest-growth channel and the biggest absolute opportunity are not the same channel. Most operators are over-rotated to digital and under-invested in offline modernisation, store experience, and unified inventory. You need a strategy — and a measurement framework — for both.

The path to purchase is no longer linear. Shoppers discover, compare, and buy across multiple platforms. Focussing on one particular channel is not sufficient.

Rajesh Jain, MD & CEO, Lacoste India

3. Has Quick Commerce Already Become India's Primary Digital Shelf?

If there is one breakout story from the entire report, it is quick commerce.

Q-commerce is live in 80+ cities with 120,000+ delivery partners. Projected to reach US$35–40 billion GMV by 2030 at a ~37% CAGR. And this number changed how I think about it: quick commerce now generates ~35% of FMCG companies’ total e-commerce revenue.

That is not a channel. That is becoming the primary digital shelf.

India is the first country where quick commerce has scaled beyond groceries — into electronics, fashion, beauty, and wellness. This is not a convenience feature. It is a structural change in what consumers expect. And once an expectation forms, it does not go back.

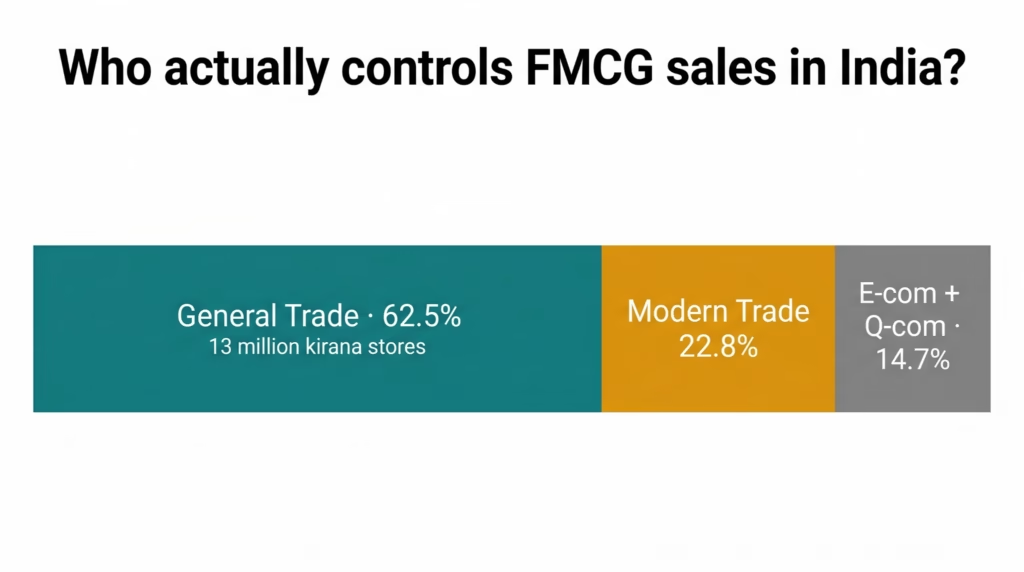

4. Are Kiranas Actually Dying — or Is Something More Interesting Happening?

India has 13 million small retailers. General trade still controls 62.5% of FMCG sales. Modern trade sits at 22.8%. E-commerce and Q-commerce together are at 14.7%.

The narrative that kiranas would be wiped out by organised retail has been around for a decade. The report tells a different story. UPI, POS systems, B2B ordering apps, and ONDC are quietly modernising this backbone — not replacing it.

The kirana was not disrupted. It was upgraded.

Brands that build distribution for the digitised kirana — smarter replenishment, digital ordering, real-time inventory visibility — will own the next decade of Bharat consumption. This is the largest distributed retail network on the planet. It is not going away. It is getting smarter.

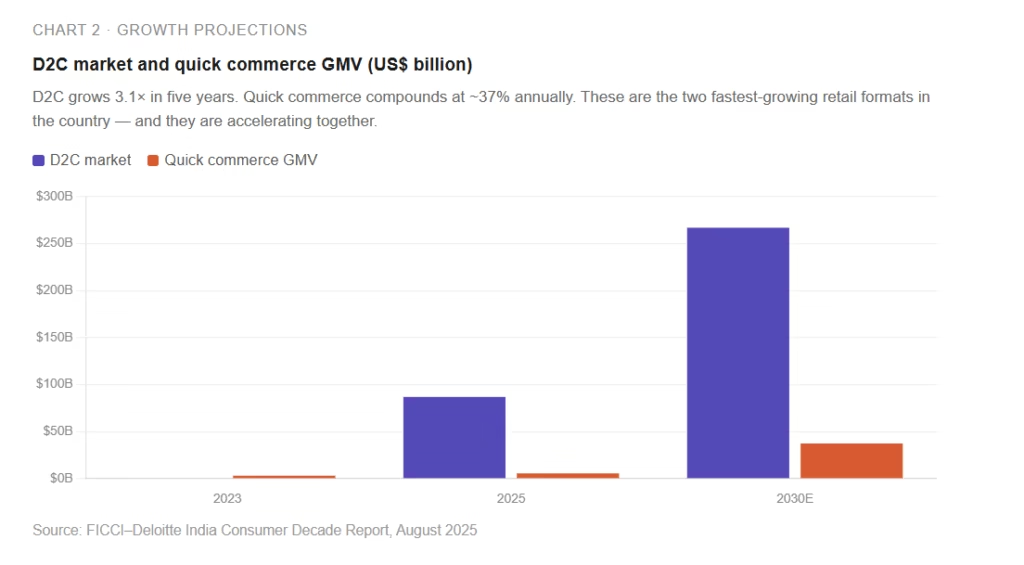

5. Is Your D2C Brand Ready for a Market That Triples to US$267 Billion?

India’s D2C market is running at a pace most brands haven’t fully priced into their strategy.

From US$87 billion in 2025 to US$267 billion by 2030 — a 3.1× growth multiple at roughly 25% CAGR. Private labels now make up 15–30% of modern retail sales and in many categories command better margins than national brands.

The playbook has shifted. Phase one of D2C was Instagram and performance ads. Phase two — the one we are in now — is omnichannel distribution, first-party data infrastructure, and private label development. Brands that cracked phase one but have not built for phase two are more vulnerable than they realise.

The M&A signal reinforces this. Tata acquired Organic India and Capital Foods. D2C brands in wellness, premium personal care, and ethnic foods are becoming acquisition targets. Scale and data infrastructure are the new entry tickets.

6. Is Bharat the Real Growth Engine Now — and Are You Building for It?

This is the insight that should change where most brands put their next rupee.

60% of e-commerce transactions now come from Tier 2 and Tier 3 cities. Rural FMCG grew 9.9% in Q4 2024 — more than twice the urban rate of 4.2%. Rural India holds 45% of the home and personal care market.

Bharat is no longer the long tail. It is the centre of gravity.

And it is not one uniform market. South India skews health-oriented. North India has different ingredient and performance expectations. East India is less saturated and emerging fast. A national rollout strategy is increasingly the wrong default.

Winning Bharat is not about the metro playbook with a discount. It is about small-unit packs, culturally relevant SKUs, and regional distribution built for how these consumers actually shop.

7. Gen Z Has US$250 Billion — Are You Speaking Their Language?

Gen Z’s direct spending hits US$250 billion in 2025. They drive nearly half of all fashion consumption in India. 65% of their fashion purchases happen online. Their collective influence — including household decisions — represents 43% of total consumer spending power.

That is not a niche. That is the market.

Authenticity beats production value. Reviews and creators outrank celebrity ads. They expect instant gratification and hyper-personalisation. They can tell the difference between a brand that stands for something and one that is performing values for marketing purposes.

This is not a segment you reach with a separate campaign. It is a different operating system.

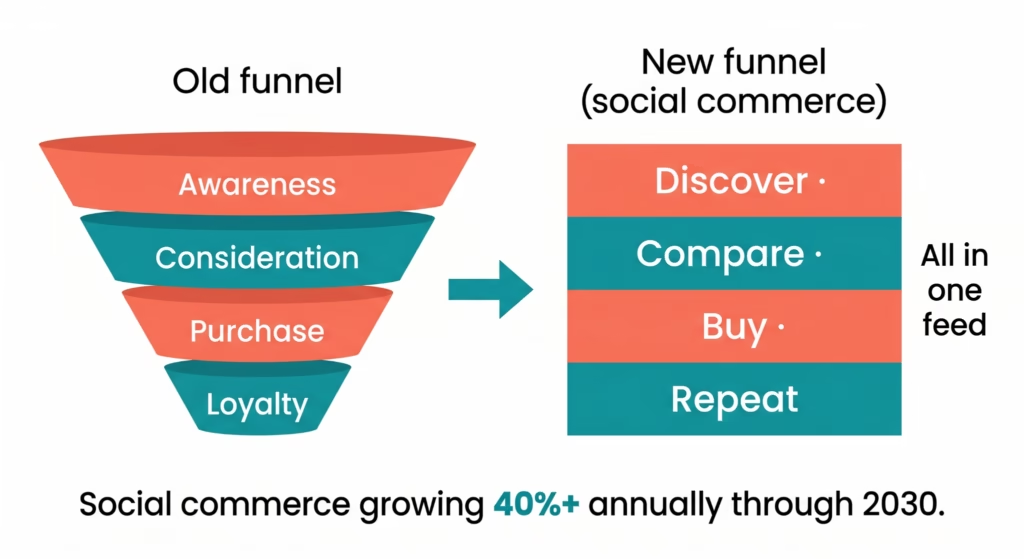

8. Social Commerce Is Growing 40%+ — Has Your Funnel Changed With It?

Social commerce — shoppable posts, live video sales, creator drops — is growing at 40%+ annually through 2030. And it is no longer just top-of-funnel.

Discovery, comparison, and purchase are collapsing into one in-app flow. A consumer sees a product in a creator’s video, taps, reads reviews, and buys — without ever leaving the platform. The funnel is the feed.

The report captures a case study of an Indian clean-skincare brand using a creator-commerce model: 30 million monthly active users, 5% conversion, marketing costs down from 75% to 30% of revenue, repeat orders up from 35% to 65%. That is not just acquisition. That is loyalty built through social commerce.

9. Premium Is Growing Twice as Fast as Mass — Are You on the Right Side of That Split?

There is a split happening in Indian consumption that most brands have not fully priced in.

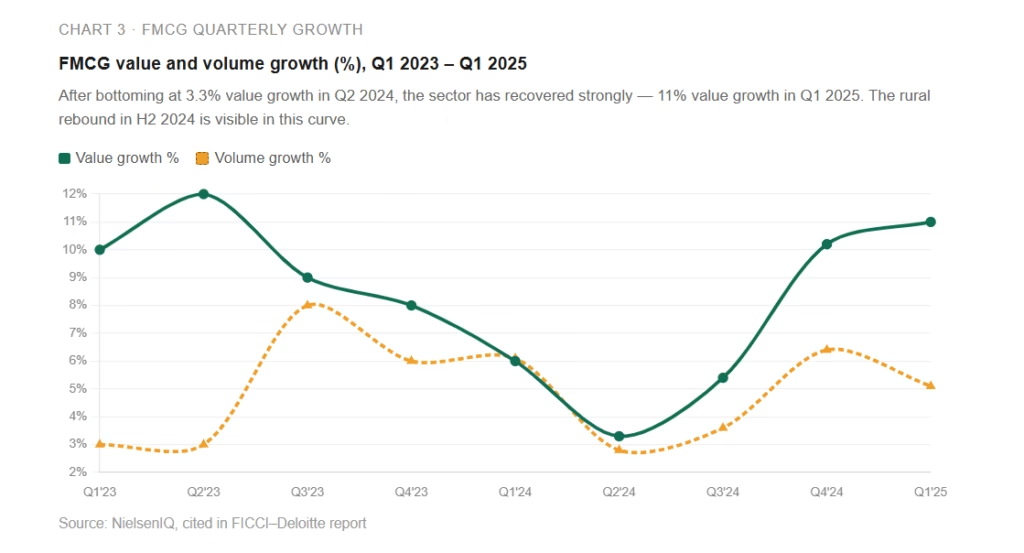

Premium FMCG ranges grow 2× faster than mass in modern retail. The top consumer quintile drives 42% of value growth. Value growth of 11% outpaced volume growth of 5.1% in Q1 2025 — pricing power is back.

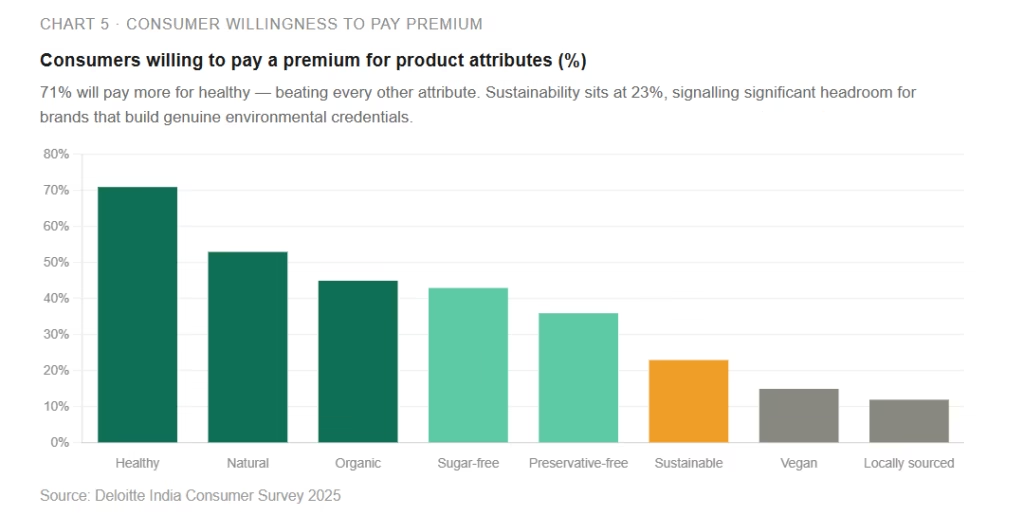

The winning lane is purpose-led premiumisation. India’s Ayurveda market alone scales from US$7 billion to US$16.27 billion by FY28. Sustainability, wellness, heritage, and self-expression are the new pricing levers. Consumers are willing to pay more — but the premium has to mean something.

10. AI, ONDC, and Omnichannel — Are These Still Pilots in Your Organisation?

Three structural shifts are underway that most brands are still treating as experiments.

AI — virtual trials, shelf image analytics, AI-driven demand forecasting — is moving from pilot to mainstream. Shiprocket’s Shunya.ai is already live for MSMEs and D2C brands. This is not future technology. It is available today.

ONDC made its first cross-border B2B order in January 2024. Small Indian manufacturers can now be export-ready through a digital catalogue. A distribution unlock that was not possible three years ago.

Omnichannel measurement is the unsexy infrastructure that determines whether any of this compounds. Offline at 9% growth. Online at 23%. Quick commerce at ~37%. Social commerce at 40%+. Four completely different growth rates, four different unit economics — most brands still report them in one P&L. That is not an analytics gap. That is a strategy gap.

The brands that win the next decade are not the ones with the most channels. They are the ones with the most accurate measurement across them.

11. Conclusion

India’s retail market doubling by 2030 is the headline. But the story behind it is ten separate shifts happening at different speeds simultaneously.

The brands that will capture the next US$865 billion are not the ones chasing the loudest trend. They are the ones who read each signal clearly — and build distinct strategies for each channel, each consumer cohort, and each geography.

The FICCI–Deloitte report does not tell you what to do. But every chart in it points to the same conclusion: measurement is the moat. The decade belongs to brands that can see clearly across all of it.

You can read the full FICCI–Deloitte India Consumer Decade Report here.

If you’d like to discuss how we can help optimise your Omnichannel Marketing strategies, feel free to reach out to us at alibha@daiom.in

For more such deep-dives and insights, follow and stay tuned to DAiOM.

Subscribe to our NEWSLETTER!