The way I shop for groceries has quietly changed over time, and I’ve noticed it most while living in Gurgaon. I used to be a regular visitor at places like D-Mart, Reliance SMART Bazaar, and Super Bazaar. That was the default way of stocking up on groceries back then.

But now, it’s different.

With the rise of quick commerce, I rarely feel the need to make those planned visits for smaller, everyday needs. While Big Box retail was the go-to, many of the small, immediate things we need are now bought directly from the neighborhood kirana stores within our society.

While my experience in a big city might reflect a shift toward digital, the broader reality for India’s mass market still leans heavily on the traditional Kirana.

Recently, I came across the The Redseer Strategy Consultants report, “Why India’s Mass Grocery Still Leans on Kiranas” and it wonderfully states the structural, economic, and behavioural reasons behind this dominance.

In this blog, we will share 3 key takeaways from the report and what they mean for brands, retailers, and marketers.

"Quick commerce is inherently a convenience-led model... The structural reality is that the bulk of Indian grocery consumption remains deeply value-driven, characterized by very small, frequent, low-ticket purchases shaped by affordability and cash-flow constraints."

Nikhil Vora, Founder & CEO, Sixth Sense Ventures

Table of Contents

1. Understanding the Indian Grocery Market

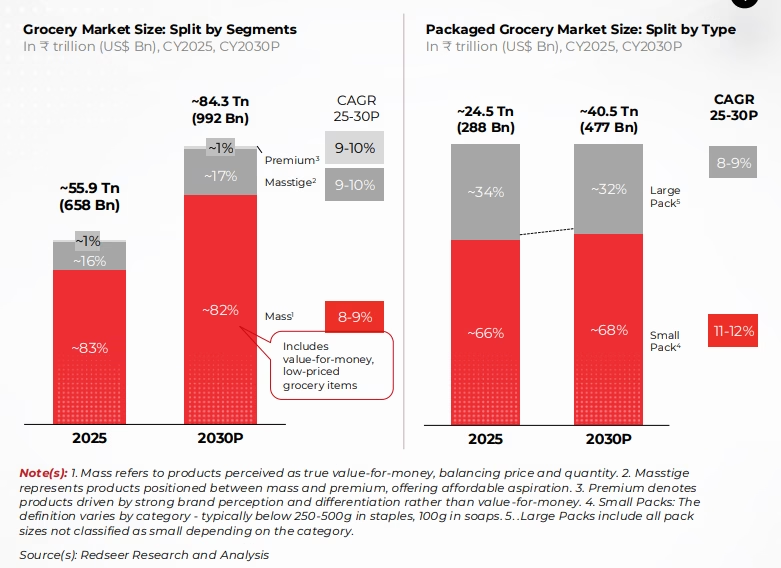

India’s grocery market is massive, essential, and deeply personal. The grocery market of India, valued at nearly ₹55.9 trillion in 2025, is expected to grow to ₹84.3 trillion by 2030, driven by rising consumption, urbanisation, and the expansion of digital and organised retail formats.

In fact, India’s grocery ecosystem is not a single market, it is a triangle of three distinct retail formats comprising kiranas, big box retail, and online commerce, each growing but serving different roles:

1.1 Big-box retail

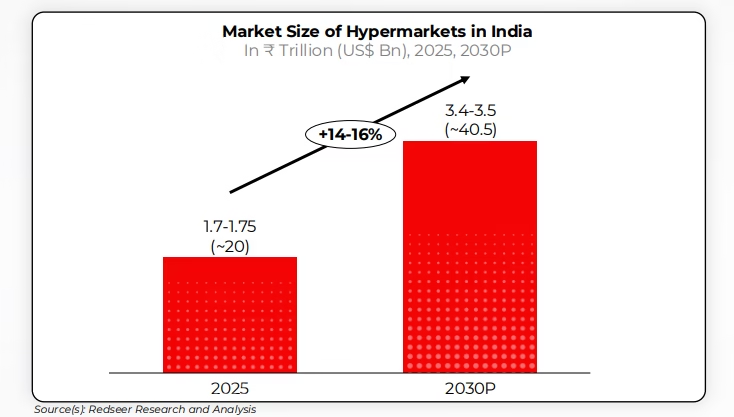

Big-box retail is often the most visible part of modern grocery shopping, especially in urban India. Valued at around $40 billion in 2025 and expected to grow to nearly $74 billion by 2030 at about 13% CAGR, this segment includes hypermarkets and supermarkets that cater to urban, upper-middle-class consumers.

These shoppers typically prefer bulk buying, structured layouts, and predictable pricing. It’s a more planned, value-driven way of shopping rather than something you rely on for daily needs.

1.2 Online grocery

Online grocery, however, is where the fastest shift is happening.

Currently a ~$19 billion market, it is projected to reach close to $69 billion by 2030, growing at an impressive 29% CAGR.

Within this, quick commerce is expanding even faster at 37–39%. The appeal is clear—speed, convenience, and doorstep delivery. But despite the rapid growth, this format is still largely limited to urban, affluent consumers who prioritize convenience and are comfortable paying a premium for it.

1.3 Kiranas

Kirana is the true backbone of India’s grocery ecosystem. With a massive market size of around $598 billion in 2025, accounting for nearly 91% of the total grocery market, kiranas continue to dominate.

Growing steadily at 7–8% CAGR, they are expected to reach about $849 billion by 2030. Their strength lies in serving India’s mass market, the middle, lower-middle, and low-income groups that make up roughly 80% of the population.

For these consumers, trust, proximity, flexible credit, and affordability matter far more than speed or scale.

Also Read: Can Brands Do Quick Commerce Without Aggregators?

While big-box and online formats are growing and evolving consumer behavior at the top end, kiranas remain at the core of how India truly shops.

2. India’s Grocery Landscape: How Each Format Serves a Different Consumer Need?

Understanding India’s grocery landscape becomes much clearer when you look at how each format is built to serve very different needs.

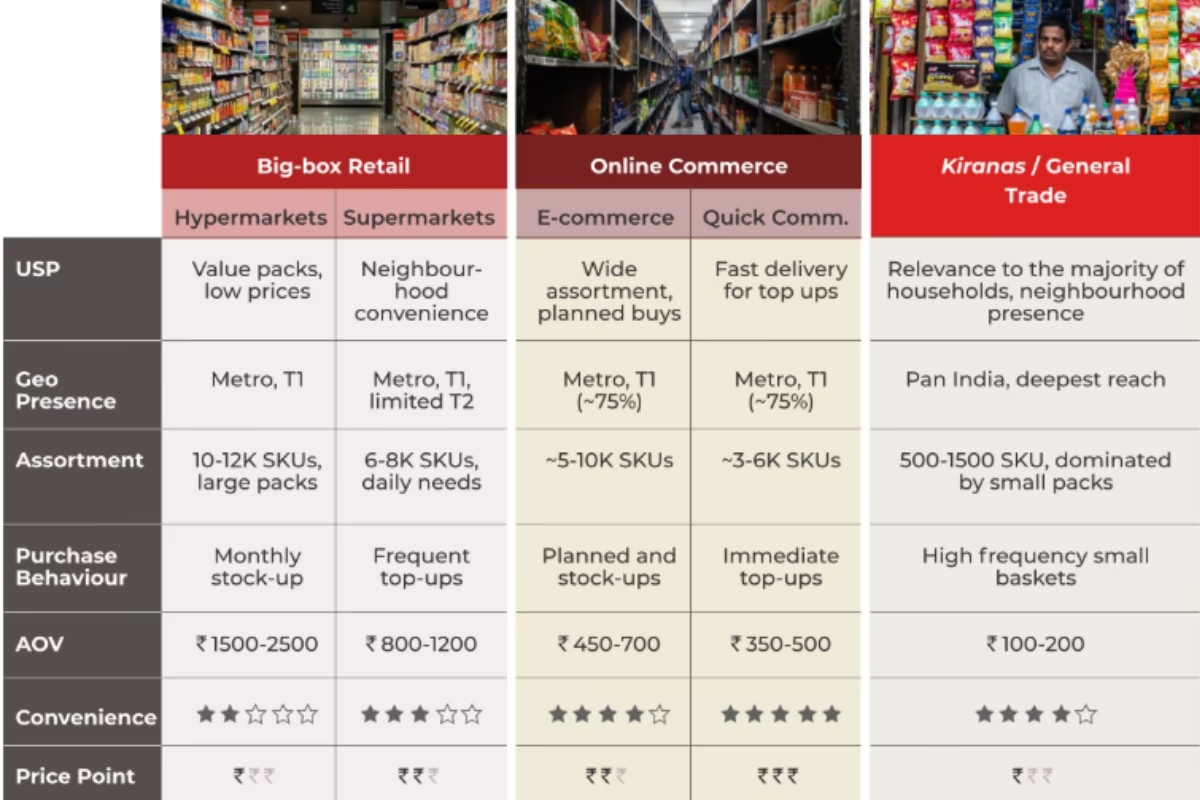

Big-box retail: Big-box retail operates on scale and planning. Hypermarkets and supermarkets focus on large assortments (up to 10–12K SKUs), bulk packs, and monthly stock-ups, which naturally leads to higher average order values.

Their presence is strongest in metros and Tier 1 cities, with limited reach beyond that. The entire experience is designed for planned shopping, consumers come in with a list, buy in bulk, and optimize for value.

Online commerce: Online commerce sits somewhere in between scale and immediacy. E-commerce platforms offer wide assortments and cater to planned purchases, while quick commerce flips that model with fast delivery and smaller baskets. Both are largely concentrated in metros and Tier 1 cities, covering roughly 75% of these urban markets.

What stands out here is the shift in purchase behavior—planned stock-ups on one end and instant top-ups on the other—driven by convenience. However, assortments are still narrower than big-box retail, and the model works best for a specific, urban consumer segment.

Kirana stores: Kirana stores are built for frequency and proximity. With a much smaller assortment (500–1500 SKUs), they focus on high-frequency, small-basket purchases with very low average order values. Their biggest strength is reach—deep, pan-India presence that no other format can match.

More importantly, they are embedded into daily life. Unlike planned or convenience-driven shopping, kiranas serve habitual, need-based consumption, often supported by trust, familiarity, and even informal credit.

3. 3 Major Trends Shaping India’s Grocery Market

From quick commerce driving new shopping habits, hypermarkets remaining strong in bulk savings, and kiranas continuing to dominate daily grocery needs across the country, here are three major trends shaping Indian grocery market:

3.1 Quick Commerce to Take the Lead in Online Grocery

Quick commerce is expanding quickly, changing how people shop. Shoppers who used to prefer e-commerce or supermarkets are now using it more.

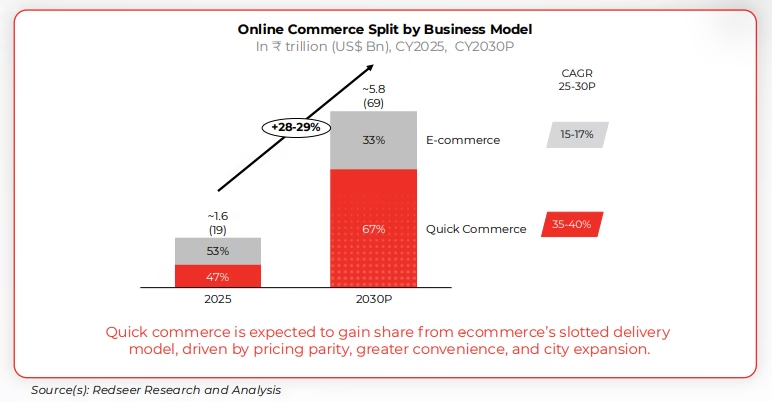

In 2025, e-commerce and quick commerce were almost evenly split, with e-commerce at 53% and quick commerce at 47% of online grocery sales (~₹1.6 trillion / US$19 Bn). By 2030, quick commerce is expected to dominate, reaching 67% of the market (~₹5.8 trillion / US$69 Bn), while e-commerce will hold 33%.

This growth is driven by faster delivery, better convenience, competitive pricing, and city expansion. Quick commerce is growing much faster than e-commerce, with a CAGR of 35–40% vs 15–17%, making it the main driver of India’s online grocery market.

On the other hand, quick commerce is rapidly changing shopping habits, attracting users who previously relied on e-commerce and supermarkets. Monthly transacting users grew ~12% by Oct ’25, driven by:

- Faster access: Dense dark-store networks and reliable, habit-driven deliveries for routine top-ups.

- Wider range: While grocery dominates (~71%), platforms are expanding into other household categories.

Moreover, quick commerce shoppers are becoming habitual, moving from impulse-driven daily fixes to planned routine top-ups. Quick commerce, once just for immediate needs, now handles planned grocery shopping too.

Affluent and mid-urban households are shifting from supermarkets and slotted e-commerce as improved reliability, assortment, and predictable delivery let quick commerce cover both top-up and weekly replenishment needs.

Also Read: India 1, 2 & 3: The Three India Framework Every Marketer Must Understand

3.2 Hypermarkets thrive on value, bulk, resisting disruption

Hypermarkets remain resilient and are projected to grow at a 14-16% CAGR, supported by their strong economic relevance for households.

Hypermarkets serve dense urban areas, with ~80,000–85,000 modern retail stores nationwide. Growth is driven by consumers moving toward organised retail, seeking better quality, wider assortments, and competitive CPG pricing.

For example, D-Mart, India’s premier hypermarket franchise, demonstrates the relevance of value and bulk savings in Indian grocery.

D-Mart grew revenue to ~₹49,300 crore in FY 2025 (+15–16% YoY), driven by groceries and essentials (~58% of sales), reflecting stable value-conscious households. Expanding to ~415 stores (~17.2 mn sq. ft), its cost-efficient, scale-driven model, strong supplier partnerships, and healthy staples-FMCG mix sustain steady same-store growth and reinforce its hypermarket advantage.

"Quick commerce has hit hypermarkets inside malls much more than standalone formats. The mall customer is already convenience-oriented and can easily shift to quick commerce. The D-Mart customer is value-first- they're willing to travel and plan their purchases to save money. That's why D- Mart hasn't seen the same kind of impact."

Arvind Mediratta, CEO & MD, Hippo Homes | Former CEO & MD, METRO Cash & Carry India

3.3 Mass Grocery Drives India’s Daily Shopping

Worth ~₹4.64 trillion (~US$546 Bn) in 2025, mass grocery reflects how Indian households manage daily spending. It is expected to remain around 82% of the market by 2030 (~₹6.4 trillion/~US$816 Bn), driven by affordability, accessibility, and frequent small purchases.

Also, kirana’s anchor mass grocery, aligned with the spending patterns of India’s largest demographic.

Alternatively, for many low- and middle-income households, small packs support daily or weekly cash flow, making frequent purchases easier. They provide access to branded goods without straining budgets and enable quick replenishment as income varies.

This price-sensitive, value-conscious behaviour keeps kiranas at the core of India’s mass grocery market. Moreover, Kirana stores run on frugality, with low-rent or owned premises, family management, and fast inventory cycles (9–10 days).

Minimal delivery and acquisition costs keep operating expenses at just 2–3%, yielding net margins comparable to organised retail. Their mix of taxable and GST-exempt items, like loose staples, gives them pricing flexibility to offer discounts and manage margins while staying compliant.

4. How Are Kiranas Modernizing Sourcing and Operations?

Kirana stores are making sourcing more planned and efficient.

- Sourcing: On the sourcing side, store owners are now coordinating with 5–10 distributors instead of relying on ad-hoc purchases. This planned approach, along with selective use of online B2B platforms, helps reduce margin leakages (around 2–5%) and ensures faster, more reliable replenishment.

- Logistics: In logistics, many kiranas are moving away from frequent wholesale market trips and instead leveraging supplier deliveries and digital ordering. This shift cuts down 3–5 hour sourcing runs, improves stock availability, and allows owners to focus more on customers and store management.

- Credit: Credit practices are also becoming more disciplined. Instead of informal, unstructured borrowing, kiranas are aligning purchases with distributor credit cycles (typically one month) and syncing inventory with real-time sales. Even when informal credit is used, they manage it more carefully to maintain steady cash flow and liquidity.

- Data and tech: Finally, on the data and tech front, adoption is gradually increasing. While many stores still rely on experience, tools like UPI and simple sales-tracking systems are helping reduce stock gaps and improve visibility into fast-moving products.

With growing digital adoption, kiranas are now refining planning, procurement, and cash-flow management, evolving from experience-led operations to more informed, flexible store management.

Improved stock availability, expanded delivery networks, and tighter replenishment cycles are making logistics easier and costs more controlled. This adaptability strengthens kiranas’ resilience, keeping them central to India’s mass-market grocery demand.

5. Conclusion

India’s grocery market is evolving, but mass grocery remains its core, driven by frequent, low-ticket purchases.

Kiranas are uniquely positioned to serve this segment, offering affordability, small-quantity purchases, curated local assortments, and lean, community-embedded operations.

While modern retail formats and online channels expand, kiranas continue to provide unmatched efficiency and relevance, remaining the irreplaceable backbone of everyday grocery consumption for the country’s largest demographic.

If you’d like to discuss how we can help optimize your Omnichannel Marketing strategies, feel free to reach out to us at alibha@daiom.in

For more insights and updates on the latest trends, follow DAiOM!

Subscribe to our Newsletter!