For most of us in India, jewellery isn’t just a product category, it’s an emotion. It’s the first gold chain from grandparents, the bridal set passed down generations, the tiny nose pin bought with your first salary. Jewellery has always lived at the intersection of culture and commerce.

Today, India’s jewellery market is valued at around ₹6,340 billion (~$75 billion) as of 2024. The scale is massive but more importantly, the market isn’t just growing, it’s transforming.

And this shift isn’t loud. It’s subtle, driven by changes in behavior, technology, and generations.

In this blog, we’ll explore how the industry is evolving and how brands need to evolve with it.

Digital in jewellery is not just a sales channel. It is the decision-making layer that feeds offline revenue.

Ashish C. Sharma

Table of Contents:

- A $75 Billion Jewellery Market of India

- Why Are People Buying Jewellery Differently Today?

- How Is India Strengthening Its Position as a Global Jewellery Leader?

- The Shift from Fragmented to Organised

- Jewellery and the Omnichannel Journey

- The Omnichannel Flywheel in Jewellery

- What are the Challenges?

- Franchise vs Owned Expansion: Strategic Choices

- Conclusion

1. A $75 Billion Jewellery Market of India

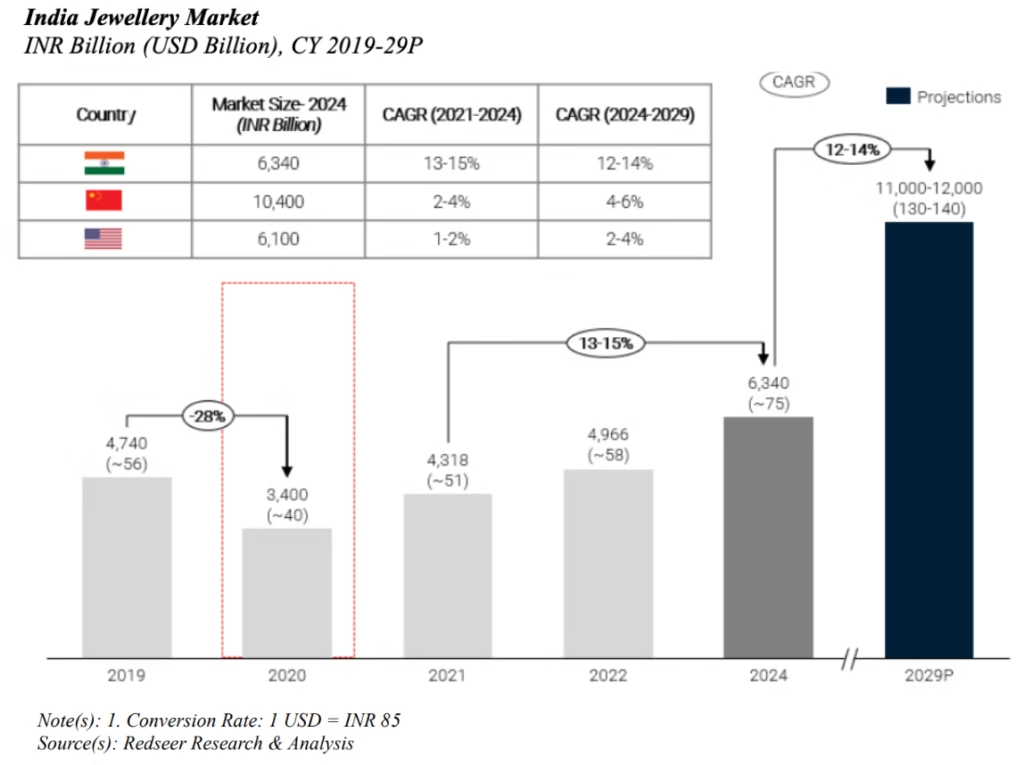

India’s jewellery market is valued at approximately ₹6,340 billion (~$75 billion) as of 2024, growing at a CAGR of 13–15% since 2021 . It has already overtaken the US to become the second-largest jewellery market globally, behind China . And it’s expected to hit ₹11,000–12,000 billion ($130–140 billion) by 2029 .

Globally, diamonds and gold together contribute nearly 70–80% of the overall jewellery opportunity, with gemstones and platinum making up the rest.

But what makes India unique is not just size, it’s heterogeneity.

This market is segmented across:

- Regions (South vs North designs are dramatically different)

- Occasions (bridal, festive, gifting, daily wear)

- Product types (necklaces, rings, bangles, studs)

- Metal/stones (22K gold, 18K studded, diamonds, lab-grown, platinum)

- City tiers (metro vs Tier II vs Tier III+)

It’s not one market. It’s many markets operating simultaneously and yet, a few powerful forces are unifying them.

2. Why Are People Buying Jewellery Differently Today?

The way Indians are buying jewellery is clearly changing, and a few powerful shifts are driving this transformation.

First, rising incomes continue to strengthen gold demand. As household incomes grow, gold remains both an ornament and a form of financial security. In India, jewellery isn’t just about looking good it’s about saving smartly. Gold still feels like safety, stability, and long-term value.

At the same time, buying behaviour is evolving:

Young urban consumers are purchasing jewellery for daily wear, office styling, gifting, and self-expression not just weddings. Diamonds, lightweight designs, and modern styles are gaining share.

Between 2016 and 2024, the share of gold jewellery declined from ~87% to ~81%, while diamonds and other metals rose from ~13% to ~19%. That shift reflects evolving taste.

Financially independent women are now primary buyers, not just influencers. They care about comfort, design, versatility, and brand trust.

Cultural occasions still matter deeply. Weddings, festivals, and religious events continue to anchor demand. Even during slowdowns, bridal jewellery remains strong.

Heavy bridal sets haven’t disappeared. But now they exist alongside minimalist studs, stackable rings, and everyday pieces.

Jewellery in India is no longer just a status symbol. It’s becoming personal, practical, and expressive while still staying rooted in tradition.

3. How Is India Strengthening Its Position as a Global Jewellery Leader?

India is not just a consumption market, it’s a manufacturing powerhouse.

The country’s karigars (artisans) bring centuries-old craftsmanship into modern retail formats. Strong skill development initiatives, jewellery parks, the Surat Diamond Bourse, and supportive policies like 100% FDI under the automatic route have modernised the ecosystem.

The BIS Hallmarking Scheme has been especially crucial. Mandatory hallmarking has increased consumer trust in purity and standardisation, something earlier generations relied on personal relationships to validate.

Then there’s the Gold Metal Loan (GML) scheme, allowing manufacturers to borrow gold instead of cash, improving working capital efficiency and reducing production volatility.

India’s jewellery strength is not accidental, it’s structured.

4. The Shift from Fragmented to Organised

Historically, India’s jewellery market was deeply fragmented. Small independent retailers dominated. Trust was hyperlocal and pricing was opaque.

But urban consumers increasingly prefer:

- Transparent pricing

- Certified purity

- Standardised quality

- Branded experiences

Organised retail is steadily gaining share, particularly in urban centres. The rise of national chains and digital-first brands has reshaped consumer expectations.

And this is where omnichannel becomes central.

4.1 Examples of Organized Jewellery Players in India

India’s organized jewellery market is led by legacy brands that have built deep trust, national scale, and strong omnichannel presence.

- Tanishq (Tata Group) continues to dominate with its extensive retail network, transparent pricing, exchange programs, and growing digital integration that connects online discovery with in-store purchase.

- Malabar Gold & Diamonds has scaled aggressively across India and international markets, combining traditional gold demand with modern store formats and structured inventory systems.

- Kalyan Jewellers has also built strong brand recall through regional marketing, celebrity endorsements, and expanding showroom footprints, while steadily investing in digital touchpoints to complement offline strength.

These brands represent organized retail at scale, where trust, purity assurance, and nationwide distribution remain the core moat.

4.2. Examples of Niche / New-Age Jewellery Brands

On the other side, new-age and niche players are reshaping the market through design innovation, digital-first strategies, and omnichannel agility.

- GIVA has built a strong position in silver and affordable jewellery by focusing on gifting, repeat purchases, and app-led retention strategies.

- Bluestone pioneered the online-first jewellery model in India and later strengthened its presence through experience stores, blending technology with physical trust-building.

- CaratLane (a Tanishq subsidiary) bridges affordability and aspirational design, leveraging strong digital marketing with an expanding offline network to drive omnichannel growth.

These brands prove that modern jewellery retail is no longer just about scale, it’s about design differentiation, digital fluency, and seamless customer journeys.

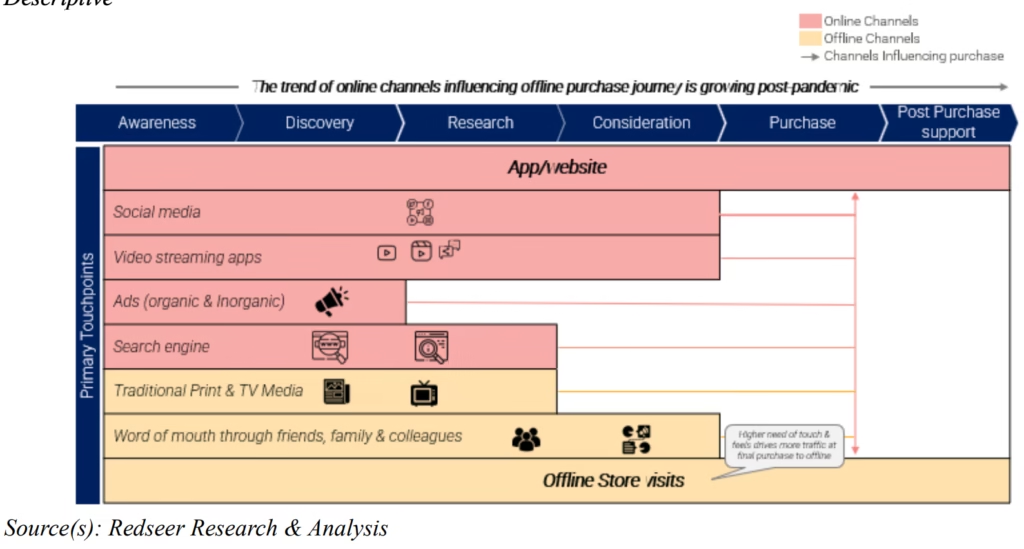

5. Jewellery and the Omnichannel Journey

If there’s one category where omnichannel truly makes a difference, it’s jewellery.

Why? Because jewellery is high-ticket and high-emotion.

Customers want:

- Online discovery

- Transparent price comparison

- Real-time inventory visibility

- Physical touch-and-feel

- Post-purchase service confidence

According to Redseer estimates, nearly 50–60% of jewellery purchases in 2024 were online-influenced. That means digital touchpoints played a role in decision-making even if the final transaction happened offline.

Consumers research online and buy offline.

The omnichannel model solves this beautifully:

- Experience centres provide touch-and-feel.

- Websites aggregate demand and enable design discovery.

- Real-time inventory sync allows planned store visits.

- CRM tools connect post-purchase engagement across channels.

When executed well, omnichannel creates a flywheel.

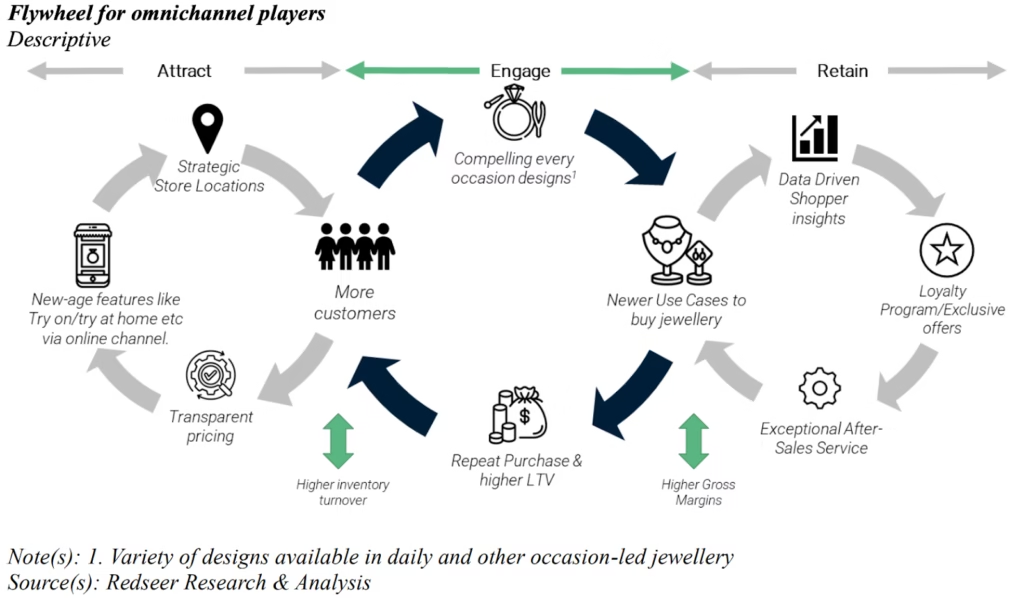

6. The Omnichannel Flywheel in Jewellery

If you look closely, jewellery growth today follows a simple but powerful three-stage cycle:

Stage 1: Attract

Brands build online awareness: Instagram ads, Google discovery, transparent pricing, design catalogues. Customers shortlist pieces digitally.

Stage 2: Engage

They visit stores, opt for in-store pickup, try-at-home services, or hybrid purchase journeys. Seamless inventory visibility prevents disappointment.

Stage 3: Retain

Loyalty programs, repair services, easy exchanges, digital reminders, occasion-based nudges. Data from online and offline touchpoints feeds back into smarter targeting.

That cycle quietly builds a stronger competitive edge over time.

It improves:

- Inventory turnover

- Gross margins

- Customer lifetime value

- Expansion strategy (using data to decide new store locations)

The brand becomes smarter with every interaction. And in jewellery, intelligence is a competitive advantage.

7. What are the Challenges?

This industry comes with its own set of real challenges.

Economic Sensitivity

Jewellery is discretionary. Economic downturns, rising interest rates, or liquidity crunches can directly impact demand.

- Gold and Diamond Price Volatility

Fluctuating global prices squeeze margins and delay purchases. Consumers shift to lighter designs or postpone buying during price peaks.

Labour Costs

Skilled artisans are essential but expensive. Retaining craftsmanship talent remains critical.

Regulatory Pressure

Import duties, taxes, hallmarking norms while improving transparency can increase compliance complexity.

Intense Competition

Players compete across pricing, quality, marketing, store experience, and digital innovation.

Supply Chain Disruptions

Geopolitical events or logistics challenges can disrupt inventory flows.

This is not an easy market. It rewards scale, trust, and operational excellence.

8. Franchise vs Owned Expansion: Strategic Choices

As brands scale offline, ownership models matter.

8.1 Complete Ownership

Full control, faster decisions, consistent experience, but high capital investment and operational burden.

8.2 Franchise Models

Lower capital intensity, faster expansion.

- FOFO (Franchise Owned, Franchise Operated) – More autonomy to franchisee but higher quality-control risk.

- FOCO/FICO (Franchise Owned/Invested, Company Operated) – Better control for the brand while reducing asset risk.

Jewellery retail requires tight control over inventory and quality. Hence, many brands prefer hybrid models to balance scale and consistency.

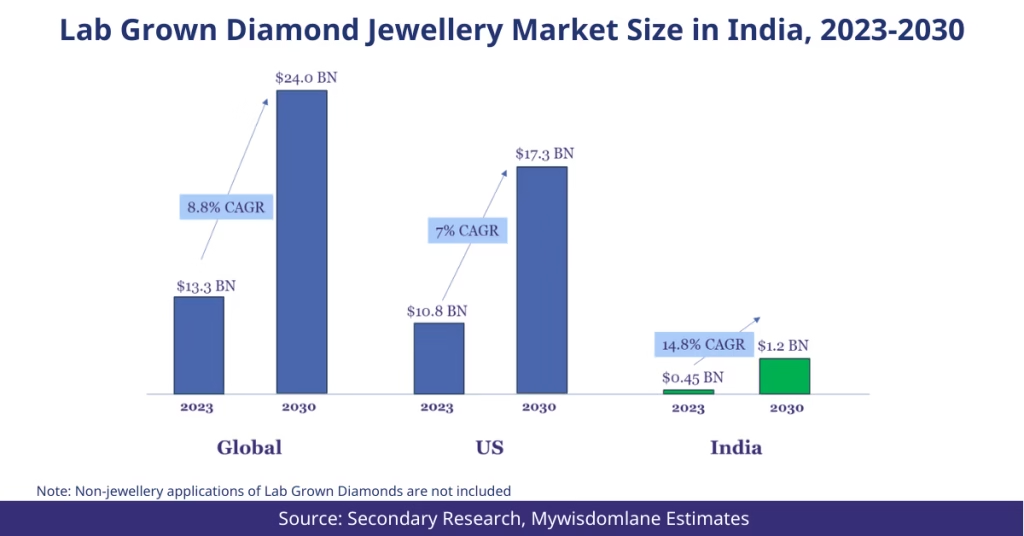

The Lab-Grown Diamond Moment

Another important structural shift is the rise of lab-grown diamonds.

They are:

- 30–40% cheaper than mined diamonds

- Physically identical

- Increasingly preferred by younger consumers valuing sustainability

Examples:

- GIVA – A fast-growing Indian jewellery brand that has actively expanded into lab-grown diamonds, making everyday diamond wear more affordable and accessible.

- Palmonas – An Indian fine jewellery brand blending contemporary design with lab-grown diamonds to appeal to modern, conscious consumers.

This category is expanding beyond niche gifting into daily wear and bridal segments. Traditional players are cautiously integrating LGD lines while educating customers on differentiation.

Discovery happens online, but shopping in India is also an experience. Digital drives discovery, but offline lets you try products, check sizing, and see how it looks.

Ishendra Agarwal, Co-Founder & CEO, GIVA

9. So Where Is This Headed?

India’s jewellery market remains heterogeneous, culturally rooted, and economically sensitive yet increasingly digital, organised, and experience-driven.

The future likely belongs to brands that:

- Treat omnichannel as infrastructure, not marketing.

- Invest in CRM intelligence deeply.

- Expand into Tier II and III cities strategically.

- Capture daily-wear growth.

- Balance gold tradition with studded and lab-grown innovation.

- Build trust through transparency and service.

Because ultimately, jewellery in India is not just about product weight or purity.

At its core, jewellery is about trust: in purity, fair pricing, reliable service, and a brand that balances emotion with integrity.

And perhaps that’s the most beautiful part of this industry.

The Indian jewellery story is no longer just about gold and tradition. It’s about data, design, experience, and meeting the consumer wherever they are.. on their phone, at a mall, or on a quick commerce app.

If you’re exploring ways to measure and communicate marketing impact more effectively, we’d love to connect. Let’s start a conversation on building omnichannel strategies for your business.

For more insights and updates on the latest trends, follow DAiOM!

Subscribe to our Newsletter!