A few years ago, buying beauty products was simple. You walked into a store, picked up what you’d seen in an ad, and trusted the brand name or maybe someone recommended the brand.

But today, we can’t buy a face wash without checking ingredients, reading reviews, watching at least two influencer videos, comparing prices across platforms, and sometimes even checking if it’s available for 15-minute delivery.

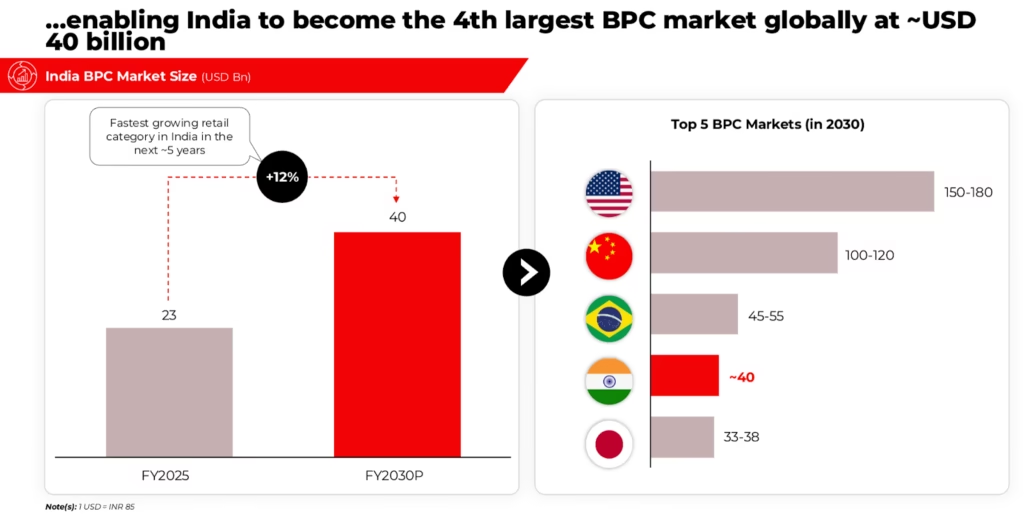

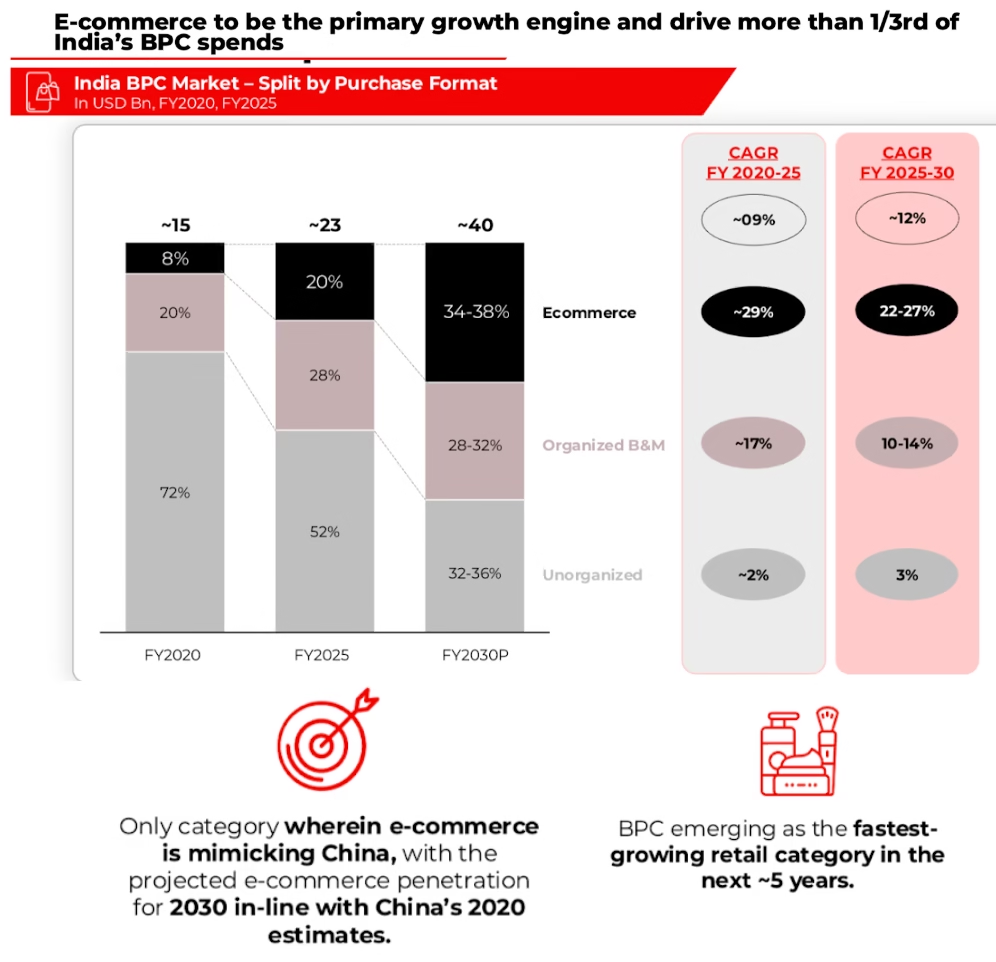

India’s beauty and personal care (BPC) market, valued at $23 billion, is set to reach $40 billion by 2030, becoming the world’s 4th largest, driven by 11%+ CAGR.

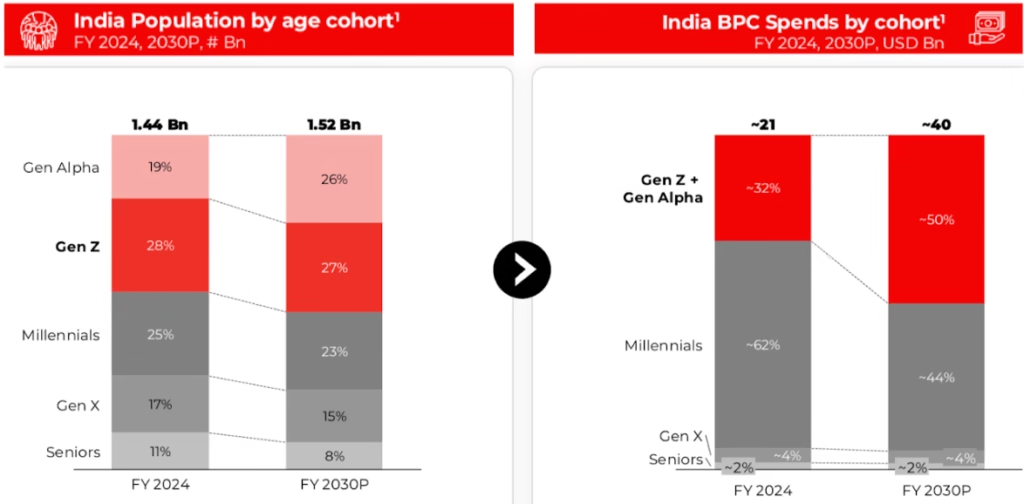

This growth is mainly fueled by Gen Z/Alpha, who will drive ~50% of spending, alongside rapid expansion in e-commerce.

The Indian beauty market isn’t just expanding in size. It’s transforming in mindset, behavior, and structure.

And if you look closely, this transformation is being driven by consumers who are more informed, more expressive, and far less patient than ever before.

Consumers are learning to ask for what they want and rightly deserve, so beauty brands have to be two steps ahead.

Rhea Sugwekar (Regulatory Researcher, June Cosmetics Solutions)

Table of Contents:

- What are the challenges?

- Is the Future of Omnichannel Data-Driven or Emotion-Led?

- Which Indian Brands Are Truly Omnichannel-First?

- Is Quick Commerce Driving the 15-Minute Beauty Revolution?

- What’s the difference between Traditional & New-age Brands?

- What’s Really Driving This Growth?

- Conclusion

1. What are the challenges?

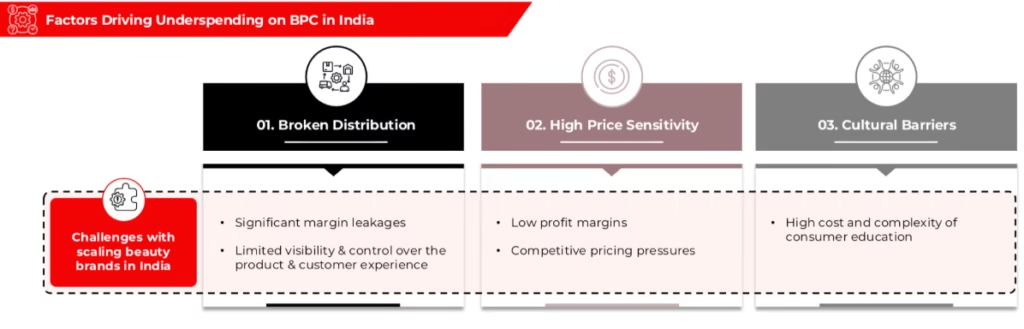

Despite strong demand, beauty and personal care (BPC) brands in India face structural challenges that make scaling difficult and often lead to underspending across the category.

1.1 Broken Distribution

Brands often deal with multiple intermediaries, which leads to significant margin leakages across the supply chain.

Beyond margins, there’s also limited visibility and control over how products are stored, displayed, priced, and experienced by customers. This makes it harder for brands to ensure consistency in quality and customer experience especially outside metro cities.

1.2 High Price Sensitivity

Indian consumers are extremely value-conscious. While demand exists, purchasing decisions are often heavily influenced by price.

This creates constant competitive pricing pressure, especially in mass and mid-premium segments. As a result, brands operate with low profit margins and must carefully balance affordability with profitability, which limits how much they can invest in marketing, innovation, or expansion.

1.3 Cultural Barriers

Beauty in India is deeply personal and culturally layered. Preferences vary by region, climate, skin tone, language, and lifestyle.

Educating consumers about ingredients, routines, or new categories requires significant investment in awareness and trust-building. The cost and complexity of consumer education can be high, particularly for new-age or premium brands introducing unfamiliar concepts.

Together, these challenges make scaling in India less about just demand creation and more about solving deep structural inefficiencies while building long-term consumer trust.

2. Is the Future of Omnichannel Data-Driven or Emotion-Led?

Beauty today is no longer just functional but It’s emotional, expressive, and deeply ingredient-led. Consumers are not simply asking, “Does this work?” They are asking more thoughtful and specific questions:

- What’s inside it?

- Is it clean?

- Is it vegan?

- Is it dermatologist-tested?

- Is it suitable for humid weather?

- Will it suit my skin tone?

By 2030, Gen Z and Gen Alpha are expected to account for nearly 50% of beauty spending in India. This generation doesn’t wait for TV ads or recommendations but they discover brands through Instagram reels, YouTube shorts, Reddit threads, and WhatsApp forwards. They validate through reviews. And they buy wherever it’s most convenient at that moment.

Sometimes the purchase happens on a D2C website. Sometimes it happens on Nykaa. Sometimes on Amazon. And increasingly, it’s happening on quick-commerce platforms like Blinkit or Zepto.

E-commerce alone is expected to account for more than one-third of total beauty spending by 2030. But even within e-commerce, no single channel dominates. D2C sites, marketplaces, vertical beauty platforms, quick commerce, and value commerce, all are growing simultaneously.

This is the time for brands to be present across channels and make every touchpoint convenient, from discovery and visibility to marketing and checkout.

Organic and natural products already command over 40% market share. Consumers care about formulations as now, they understand active ingredients like niacinamide and salicylic acid. They follow skincare routines instead of buying single products.

Beauty has moved from product purchase to self-care ritual.

And brands that understand this shift are building much deeper relationships with their customers.

3. Which Indian Brands Are Truly Omnichannel-First?

India’s most successful consumer brands aren’t choosing between online and offline anymore, they’re building seamless journeys across both.

The real differentiator today isn’t presence on multiple channels, but how consumer-centric and connected those channels feel.

3.1 Nykaa

If one company changed how Indians shop for beauty, it’s Nykaa.

Nykaa didn’t just sell cosmetics. It built trust in a market that had counterfeit issues and limited global access. It led with education, blogs, tutorials, ingredient breakdowns…long before pushing hard on commerce.

Today, it has:

- Over 9,000 brands on its platform

- 200+ physical stores

- 35 million annual transacting customers

- Rapid delivery formats like Nykaa Now

What Nykaa mastered is omnichannel.

Customers discover online, they try offline and then they reorder through apps. The data flows across systems. Inventory decisions are informed by purchase behavior. Offline stores don’t compete with online but they complement it.

Nykaa is the backbone of India’s modern beauty shopping behavior.

3.2 Mamaearth

Mamaearth started with a simple promise: safe, toxin-free products for babies.

From there, it expanded into skincare, haircare, and beyond. It grew fast, powered by digital marketing and influencer collaborations.

After that, they decided to scale offline aggressively. Through “Project Neev,” Honasa (Mamaearth’s parent company) restructured its offline distribution by replacing partners, improving direct billing, and resetting supply chains.

Today, Mamaearth is present in over 1 lakh retail touchpoints and plans to expand further. Nearly 60% of its revenue is projected to come from offline channels in the future.

Digital discovery builds brands but offline presence builds scale.

3.3 Sugar Cosmetics

Sugar Cosmetics spends almost all its marketing budget online on Instagram, influencers, YouTube and that’s where awareness is built.

Yet, a majority of its revenue comes from offline stores.

That is because beauty is tactile. People like to try shades and feel textures and Sugar understood this early.

With presence across 40,000+ outlets and strong Tier II & III expansion, it has cracked something important: digital drives traffic, stores drive trust and higher basket size.

That’s omnichannel done right.

3.4 mCaffeine

mCaffeine created a niche as “caffeine-based personal care”.

Coffee-infused scrubs and serums stood out in a crowded “natural” category. It built a strong identity around one ingredient.

The brand grew online first, but is now expanding offline selectively. It’s honest about the challenges of retail scaling and is careful about store expansion.

Beauty startups are learning that profitability matters as much as growth.

3.5 Plum

Plum may be one of the most disciplined players in the space.

One of India’s early vegan beauty brands, Plum balances online and offline almost evenly. It has scaled carefully, improved margins, and focused on premium positioning.

In a market where many brands chase aggressive expansion, Plum’s approach shows maturity.

The Indian beauty market is no longer about reckless growth it’s about sustainable omnichannel building.

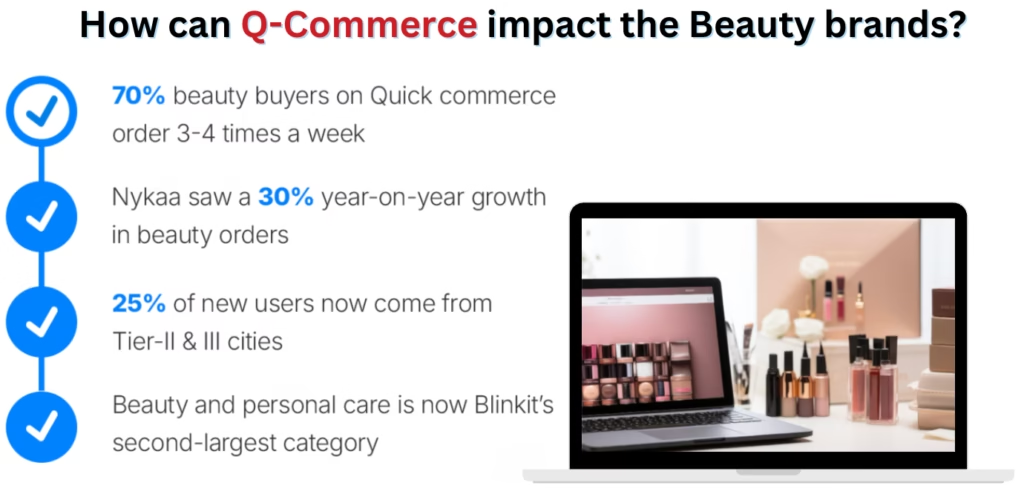

4. Is Quick Commerce Driving the 15-Minute Beauty Revolution?

Quick commerce platforms like Blinkit and Zepto are not just grocery apps anymore. Beauty is one of their fastest-growing categories.

Imagine, you’re getting ready for a party and realize you need a new lipstick. Instead of planning a mall visit, you order it in 15 minutes.

That impulse moment used to belong to physical stores. Now it belongs to dark stores.

For brands, this means:

- Another distribution channel

- Another inventory layer

- Another data stream

And it’s growing fast, as demand is expanding beyond, and beauty has become a top category on instant delivery apps, signalling a major shift in how and where consumers shop.

5. What’s the difference between Traditional & New-age Brands?

The legacy players built scale through distribution strength and mass marketing and emerging brands are building influence through content, community, and data. The playbooks are different but increasingly, they’re starting to overlap.

Let’s simplify the difference.

Traditional beauty brands such as Himalaya, Lotus herbals & Biotique:

- Led with mass marketing

- Focused on functionality

- Relied heavily on general trade

- Limited ingredient transparency

New-age brands such as Minimalist, Mamaearth & Sugar Cosmetics:

- Lead with content and community

- Talk about ingredients and routines

- Use D2C + marketplaces + quick commerce

- Leverage first-party customer data

- Build strong influencer ecosystems

But now traditional FMCG giants are learning fast. They are acquiring D2C brands, investing in digital, and building their own innovation labs.

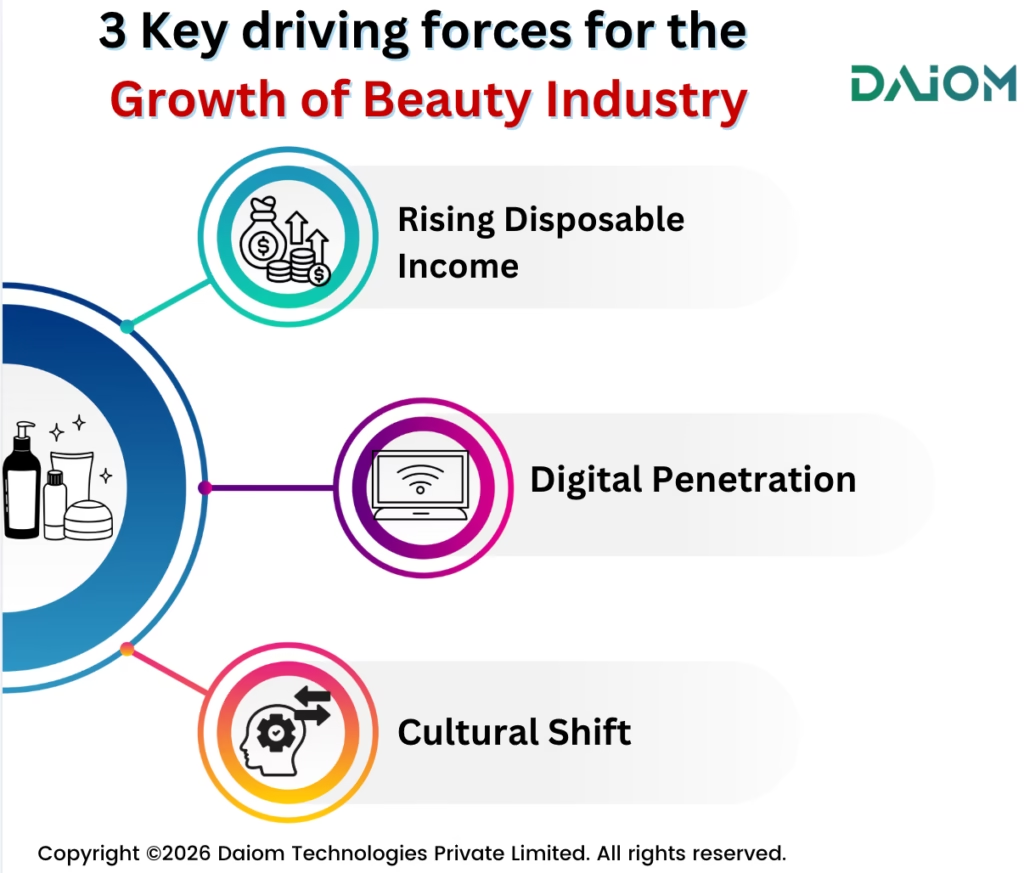

6. What’s Really Driving This?

If you look at the bigger picture, three key forces are driving the growth of this industry.

- Rising Disposable Income: Consumers are willing to trade up.

- Digital Penetration: Affordable smartphones and data access have democratized discovery.

- Cultural Shift: Beauty is no longer vanity but it’s self-expression and self-care.

India historically under-spent on beauty compared to global averages and that gap is now closing.

The Omnichannel Reality:

What makes the Indian beauty market especially unique today is that no single channel dominates the journey. D2C websites matter. Marketplaces matter. Nykaa plays a strong role. Offline stores still influence decisions. Quick commerce is rising rapidly.

And through all of this, they expect the experience to feel seamless.

That seamless, omnichannel expectation is no longer a differentiator. It’s the new baseline.

7. What’s Next?

From a world where choices were limited to a handful of brands, we now have thousands of options. From a time when ads dictated buying, now creators and communities influence decisions. From offline-only dominance, we now have a truly omnichannel ecosystem.

This isn’t just industry growth but it’s consumer empowerment.

Beauty today isn’t about hiding flaws, it’s about expressing identity. And the brands that respect that; that build transparent products, meaningful experiences, and seamless journeys, are the ones shaping the future.

Looking ahead, a few things are clear:

- Premiumization will continue.

- Tier II and III cities will drive the next wave.

- Ingredient-led and Ayurveda-meets-science brands will grow.

- Profitability will matter more than just valuations.

- Content and community will remain the biggest moat.

The brands that win won’t just be the loudest.

They’ll be the ones that understand how discovery, convenience, trust, and data connect together.

If you’d like to discuss how we can help optimize your Omnichannel Marketing strategies, feel free to reach out to us at alibha@daiom.in

For more insights and updates on the latest trends, follow DAiOM!

Subscribe to our Newsletter!